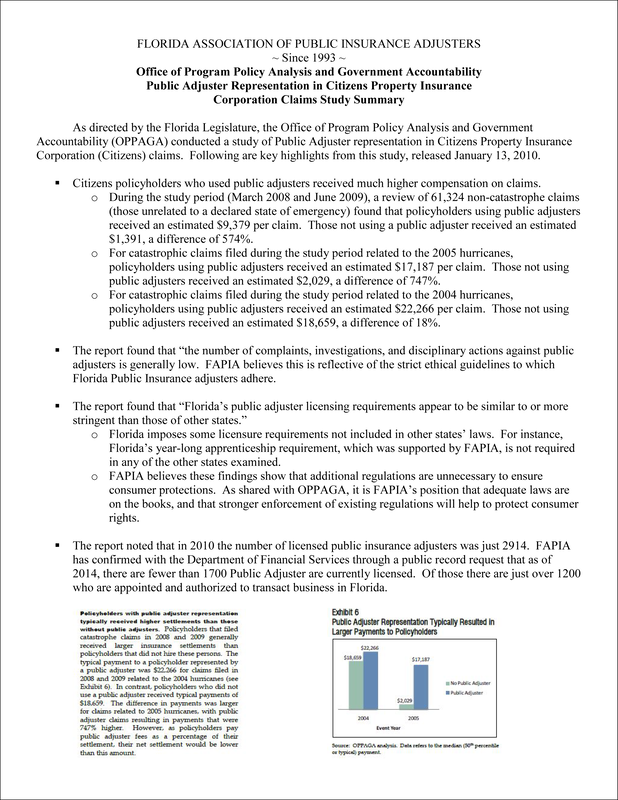

PUBLIC INSURANCE ADJUSTER

A LICENSED PROFESSIONAL

Protecting Policyholders and Their Claims

WHEN PEOPLE’S HOMES OR BUSINESSES ARE LOST TO FIRE, HURRICANE, OR OTHER INCIDENT, THE PROCESS OF NAVIGATING INSURANCE CLAIMS AND RECOVERY CAN BE DIFFICULT AND EMOTIONALLY DRAINING. MOREOVER, WITHOUT THE EXPERTISE IN FILING A CLAIM, CONSUMERS OFTEN ARE AT AN EXTREME DISADVANTAGE.